Cashless Economy?

What is a Cashless Economy?

Cashless Economy can be defined as a situation in which the flow of cash within an economy is non-existent and all transactions must be through electronic channels such as direct debit, credit cards, debit cards, electronic clearing, and payment systems such as Immediate Payment Service (IMPS), National Electronic Funds Transfer (NEFT) and Real-Time Gross Settlement (RTGS) in India.

For the financial year 2019-20, the tax deduction for cash withdrawal exceeding 1 crore will be 2% as a part of leveraging the concept cashless economy. Businesses with an annual turnover of over Rs 50 crore are entitled to offer low-cost digital modes of payments and they won’t have to incur extra charges on Merchant Discount Rate. As the digital mode of payment is overtaking the liquid cash transaction method, the Reserve Bank of India has to incur very fewer charges on maintaining the cash. This ultimately will help in having a positive cash flow in the economy.

Highlights of Cashless Economy in India

- Post Demonetization, the Centre is making a big push for online and card-based transactions in the country to achieve its target of becoming a largely cashless economy.

- The rapid growth of e-payment startups in the country.

- Launch of Unified Payments Interface (UPI) to facilitate cashless transactions.

Cashless Economy – Types of Cashless Modes and Payments

There are various cashless payment modes and these are mentioned below:

| Mobile Wallet | Plastic Money. | Net Banking |

Mobile wallet: It is basically a virtual wallet available on your mobile phone. You can store cash in your mobile to make online or offline payments. Various service providers offer these wallets via mobile apps, which is to be downloaded on the phone. You can transfer the money into these wallets online using credit/debit card or Net banking. This means that every time you pay a bill or make a purchase online via the wallet, you won’t have to furnish your card details. You can use these to pay bills and make online purchases.

Plastic money: It includes credit, debit and prepaid cards. The latter can be issued by banks or non-banks and it can be physical or virtual. These can be bought and recharged online via Net banking and can be used to make online or point-of-sale (PoS) purchases, even given as gift cards. Cards are used for three primary purposes – for withdrawing money from ATMs, making online payments and swiping for purchases or payments at PoS terminals at merchant outlets like shops, restaurants, fuel pumps etc.

Net banking: It does not involve any wallet and is simply a method of online transfer of funds from one bank account to another bank account, credit card, or a third party. You can do it through a computer or mobile phone. Log in to your bank account on the internet and transfer money via national electronic funds transfer (NEFT), real-time gross settlement (RTGS) or immediate payment service (IMPS), all of which come at a nominal transaction cost.

Cashless Economy – Prepaid Payment Instrument

The RBI classifies every mode of cashless fund transfer using cards or mobile phones as ‘prepaid payment instrument’. They can be issued as smart cards, magnetic stripe cards, Net accounts, Net wallets, mobile accounts, mobile wallets or paper vouchers. They are classified into four types:

- Open Wallets: These allow you to buy goods and services, withdraw cash at ATMs or banks and transfer funds. These services can only be jointly launched in association with a bank. Apart from the usual merchant payments, it also allows you to send money to any mobile number linked with a bank account. M-Pesa by Vodafone is an example.

- Semi-Open Wallets: You cannot withdraw cash or get it back from these wallets. In this case, a customer has to spend what he loads. For example, Airtel Money/Ola Money is a semi-open wallet, which allows you to transact with merchants having a contract with Airtel/Ola.

- Closed Wallets: This is quite popular with e-commerce companies; wherein a certain amount of money is locked with the merchant in case of a cancellation or return of the product or gift cards. Flipkart and Book My Show wallets are an example.

- Semi-Closed Wallets: These wallets do not permit cash withdrawals or redemption, but it allows you to buy goods and services from listed vendors and perform financial services at listed locations. Paytm is an example.

Advantages of a Cashless Economy in India

- Tackling Black Money: The main advantage of a cashless society is that a record of all economic transactions through electronic means makes it almost impossible to sustain black economies or underground markets that often prove damaging to national economies. This reduces the chances of black money entering the system. It is also much riskier to conduct criminal transactions. An economy that is largely cash-based facilitates a rampant underground market which abets criminal activities such as drug trafficking, human trafficking, terrorism, extortion etc. Cashless transactions make it difficult to launder money for such nefarious activities.

- Circulation of Fake Currency notes can be curbed.

- A cashless economy will help reduce corruption.

- Increase Tax base: It is difficult to avoid the proper payment of due taxes in a cashless society, such violations are likely to be greatly reduced.

- The increased tax base would result in greater revenue for the state and greater amount available to fund the welfare programmes.

- Digital transactions bring in better transparency, scalability and accountability.

- Digital transactions are convenient and improve market efficiency

- Transaction costs will come down in the long run

- It would bring down the logistics & cost involved in printing, managing and moving money around.

- It will eliminate the risks associated with carrying and transporting huge amounts of cash

- The cashless economy will reduce the production of paper currency and coins. This will save a lot of production cost in turn.

- A lot of data transfer happens due to the cashless transaction. This data will help the government plan for future expenses such as housing, energy management, etc from the pattern of the data transmission.

Challenges in transitioning to a Cashless society

- Acceptance infrastructure and digital inclusion: Lack of adequate infrastructure is a major hurdle in setting up a cashless economy. Inefficient banking systems, poor digital infrastructure, poor internet connectivity, lack of robust digital payment interface and poor penetration of PoS terminals are some of the issues that need to be overcome. Increasing smartphone penetration, boosting internet connectivity and building a secure, seamless payments infrastructure is a prerequisite to transition into a cashless economy.

- Financial Inclusion – For a cashless economy to take off the primary precondition that should exist is that there should be universal financial inclusion. Every individual must have access to banking facilities and should hold a bank account with debit/credit card and online banking facilities.

- Digital and Financial Literacy – Ensuring financial and digital inclusion alone are not sufficient to transition to a cashless economy. The citizens should also be made aware of the financial and digital instruments available and how to transact using them.

- Cyber Security – Digital infrastructure is highly vulnerable to cyber-attacks, cyber frauds, phishing and identity theft. Off late cyber-attacks have become more sophisticated and organised and poses a clear and present danger. Hence establishing secure and resilient payment interfaces is a prerequisite for going cashless. This includes enhanced defences against attacks, data protection, addressing privacy concerns, robust surveillance to pre-empt attacks and institutionalised cybersecurity architecture.

- Changing habits and attitude – Indian economy functions primarily on cash due to lack of penetration of e-payment modes, digital illiteracy of e-payment and cashless transaction methods and thirdly habit of handling cash as a convenience. In this scenario, the ideal thing to do is to make people adopt e-payments in an incremental fashion and spread awareness to initiate behavioural change in habits and attitude.

- Urban-Rural Divide – While urban centres mostly enjoy high-speed internet connectivity, semi-urban and rural areas are deprived of a stable net connection. Therefore, even though India has more than 200 million smartphones, it is still some time away for rural India to seamlessly transact through mobile phones. Even with regard to the presence of ATM’s, PoS terminals and bank branches there exists a significant urban-rural divide and bridging this gap is a must to enable a cashless economy.

Is India Ready for a cashless economy?

India’s reliance on cash

- Indian economy is primarily to be driven by the use of cash and less than 5% of all payments happen electronically. This is largely due to the lack of access to the formal banking system for a large part of the population and as well as cash being the only means available for many. Large and small transactions continue to be carried out via cash. Even those who can use electronic payments, use cash.

- Indians traditionally prefer to spend and save in cash and a vast majority of the more than 1.2 billion population doesn’t even have a bank account.

- Indian economy is primarily driven by the informal sector, and it relies heavily on cash-based transactions.

- A report by Google India and Boston Consulting Group showed that IN 2015 around 75% of transactions in India were cash-based while in developed countries like USA, Japan, France, Germany etc. it was just around 20-25%.

- RBI estimates for July 2016 show that banks had issued around 697.2 million debit cards and 25.9 million credit cards to customers after deducting withdrawn or cancelled cards. However, cards on their own cannot turn the economy into a cashless one. It is important to note that the number of cards in operation is not equal to the number of individuals holding those cards. It basically means that many customers hold multiple accounts and cards.

- The difficulty in going digital is exemplified by the data on debit card usage — over 85% (in volume) and 94% (in value) of all debit card usage is at ATMs for the purpose of withdrawing cash. The principal purpose for cards in an Indian context is thus a means to withdraw cash. The exponential growth in debit cards (over 600 million) is a direct consequence of the financial inclusion drive that led to the opening of over 170 million bank accounts. Though the move put plastic money into the hands of millions, effectively it has only shifted cash withdrawals from banks to ATMs, which was not quite the intent.

India’s Cash to GDP ratio:

As calls for going cashless grows louder in India, a key challenge being faced at the global level is to check the continuing rise in the total value of the currency in circulation and its share in the overall GDP, a trend particularly seen in the US, Switzerland and Euro area.

Such a continuing rise in the circulation of currencies for economic activities could well be a major impediment in the transformation to a cashless and digital economy.

India’s cash to GDP ratio — an indicator of the amount of cash being used in the economy — is around 12 to 13%, which is much higher than major economies including the US, the UK and Euro area but below that of Japan (about 18%).

Surprisingly Indonesia, another developing economy, has a much lower ratio of around 5%.

Cashless Economy in India & The Challenges ahead:

The biggest roadblock India faces in setting up a cashless economy is with regard to Digital and Banking Infrastructure, Security and Literacy. Most of the cash transactions in the country are small exchanges for goods or services and the penetration of PoS terminals is just not enough. Millions of people still don’t have a bank account, access to PoS terminals, internet or awareness to understand and use online payment methods etc. So we need a large scale penetration of digital services and PoS terminals to facilitate digital transactions in small towns, rural areas, untapped markets in urban India. The main question that arises is “Are digital payments secure enough for the Indian economy to go cashless?”

- Universal Financial Inclusion – Despite the success of Jan Dhan Yojana in improving financial inclusion, it has been found that most accounts have been dormant. 23% of PMJDY accounts lie empty and have been labelled as zero-balance accounts.

- Card acceptance infrastructure – India struggles to keep pace with its growing population, in 2014, there were just 18 ATMs and 13 commercial bank branches for every 100,000 adults – in comparison; the number in Brazil was 129 and 47 respectively. From 2013 to 2015, debit cards grew twice as fast as the number of PoS terminals and 1.5 times the number of ATMs, with the majority of the new infrastructure taking root in urban centres. There are at least 1.45 million PoS terminals set up by banks across the country with over 2 lakh ATMs. But, the retail locations for PoS transactions is nowhere near to the over the counter cash transactions. India’s modern banking system maps neatly onto social and spatial inequalities. Only 18% of all ATMs are deployed in rural India. The RBI’s own research finds that the states with a higher female population and a more rural populace showed lower levels of financial inclusion.

- Consumer Behaviour & Financial Literacy: Common man finds the usage of cards, mobile banking and PoS terminals to be a complex process. This requires large scale literacy and awareness campaigns to be run across the country.

- Low Penetration of Mobile Banking: The impact of mobile wallets in hastening the transition to a cashless economy is clearly overstated. Merely 26% of India has internet access, and there are only 200 million users of digital payment services. The World Bank’s Global Findex clearly shows that Indians are significantly less familiar with digital banking – in the use of credit or debit cards, in transacting using mobile phones and using net banking to pay bills – than their peers in middle-income nations.

- Poor Internet Connectivity: Despite the exponential surge in mobile penetration, India is riddled with below par internet connectivity and electricity shortage. The Indian government had pegged the ‘JAM Trinity’ as the building block towards a less-cash future. But data suggests that India still has a long way to go in efficiently linking bank accounts with mobile numbers. Also, a clear urban-rural divide exists in this regard.

Penetration of Mobile Accounts

- Securing the digital gateways: Banking infrastructure is wide open to compromise and that has been witnessed on multiple occasions in recent years. In October 2016, 3.2 million debit card details belonging to multiple Indian banks were hacked. The breach is said to have originated in malware introduced in systems of Hitachi Payment Services, which enabled fraudsters to access information allowing them to steal funds. Cyber-attacks have become increasingly difficult to curb and the focus needs to also be on drafting strong legislation to guarantee digital privacy and data security. Individuals must be allowed more control over their data, conditional access to data indicating user behaviour etc.

- Privacy Concerns: The potential loss of privacy is an obvious concern that comes with a cashless economy. Possibilities of personal surveillance and electronic snooping, as well as profiling without consent, have been pointed out by many. A cashless society can potentially give the government of the day unprecedented access to information and power over the citizens and would require strong technical and legal frameworks to guard against misuse of power. The problem is compounded by the fact that data protection laws and public policies often lag way behind technology anywhere in the world. In India, privacy is not a major concern and there is a lack of privacy or data protection laws.

It would require a fair amount of informed debate before the privacy concerns of citizens can be properly worked out, and it will definitely be premature to consider going cashless before that can happen. The government needs to clearly spell out the technical standards and the regulatory measures required to ensure the protection of privacy of its citizens, even from itself. The possibility of electronic mass surveillance on all monetary transactions does not augur well for civil liberty and democracy.

Cashless Economy – Changing Trends

Cash is all set to loose currency in India, as an explosion in smartphone usage is driving a digital payments boom. By 2020, nearly $500 billion worth of transactions in India will happen digitally via online wallets and other digital payment systems which is 10 times the level currently, according to a report by Google India and The Boston Consulting Group.

But the excessive reliance on notes and coins in India is likely to diminish, as spending habits and attitudes change and financial services reach out to more people. A sharp surge in the use of mobile phones with internet connectivity will help drive the transition to digital payments, said the report. India currently has more than 1 billion mobile subscribers, 25% of whom use smartphones, according to the report. By 2020, the number of smartphone users in the country will likely be around 520 million, and the number of internet users will be approximately 650 million, twice the current numbers, according to the report.

Personal net banking has become more popular in India off late along with digital payment options that allow users to pay mobile phone, electricity and even taxi bills. The recent spurt of growth has come from non-banking companies offering payment services. ISP’s like Airtel and Vodafone offer facilities to transfer money using phones, while “wallet” startups like Paytm and MobiKwik, allow users to load and store money digitally and pay transact through their payment interfaces.

The next level of growth will come when local mom-and-pop/Kirana grocery stores start accepting digital payments. While cash remains the most preferred choice, there has been a big build-up in the digital payments infrastructure. Cashless payments are helping overcome the severe liquidity crunch that the Indian economy is facing post demonetization. The government’s initiatives over the past year or so have been focused on promoting e-payments, plastic transactions, and cashless payments. It is true indeed, the future for the Indian economy.

Cashless Economy and Government Initiatives

- UPI: India’s biggest and boldest payments interface bet yet

What is UPI?

Unified Payments Interface has been launched by National Payments Corporation of India (NPCI) to further RBI’s vision of transitioning towards a “less-cash” and more digital society. A set of standard application programming interfaces (APIs) provide an interoperable system for seamless transfers, and it has been built on top of the immediate payment service (IMPS) platform. The UPI ecosystem functions with 3 key players:

- Payment service providers (PSPs) to provide the interface between the payer and the payee. Unlike wallets, here the payer and the payee can use two different PSPs.

- Banks will provide the underlying accounts. In some cases, the bank and the PSP may be the same.

- NPCI will act as the central switch by ensuring Virtual Payment Address (VPA) resolution, affecting credit and debit transactions through IMPS.

How does it work?

UPI which is built on IMPS allows payment directly from your bank account in real-time. There is no need to pre-load money in your wallets. It allows for payments to different merchants and vendors without the hassle of typing card details or net-banking password. Money transfers with this interface are secured with the two-factor authentications as mandated by the RBI: your mobile phone handset constitutes the first factor and the mobile PIN is the second.

Is UPI better than cards?

UPI will bring in low cost, high-volume payments and help create a new ecosystem where customers and merchants will come together for faster and simpler electronic payments. It is likely to benefit the overall payments ecosystem, as the payments service can be provided by banks to the merchant with an entry-level smartphone and it does not require a PoS machine. Thus, it is likely to reduce the overall merchant acquisition and operating cost for the banks.

The most important feature of UPI is its open architecture. The user interface is highly flexible and banks have the freedom to create the most intuitive interface. The innovation will also bring all key stakeholders on a common platform and will help create a plethora of services that are unheard of in today’s global payment offerings.

The success of UPI is basically dependent on the adoption of the platform by all banks. Further, a user needs to have a smartphone to make a transfer and hence the potential user base will be restricted to around 240 million people as of now.

- NITI Aayog Committee

- The Centre has set up a committee headed by NITI Aayog CEO Amitabh Kant, to formulate a strategy to expedite the process of transforming India into a cashless economy.

- The panel is tasked with identifying various bottlenecks that are affecting access to digital payments.

- The committee has been asked to identify and operationalise in the earliest possible time frame user-friendly digital payment options in all sectors of the economy. This is an integral component of the government’s strategy to transform India into a cashless economy

- The panel will engage regularly with all stakeholders – Central ministries, regulators, state governments, district administration, local bodies, trade and industry associations to promote adoption of digital payment systems.

- The idea is to establish and monitor an implementation framework with strict timelines to ensure that nearly 80% of the transactions in India moves to the digital-only platform

- The committee will also try to estimate the costs involved in various digital payments options and oversee the implementation of these measures to make such transactions between the government and citizens cheaper than cash-based transactions.

- The Centre is also working towards moving all government transactions to the cashless mode, through a new single-window e-payment system that individuals or businesses can use to make payments to any central or state agency.

- During the first meeting of the committee, it was decided to utilize existing Common Service Centres to help train merchants to use digital payment methods.

- Panel of Chief Ministers

- The Centre has announced the setting up of a 13-member committee, which includes 6 Chief Ministers, to come up with an action plan to rapidly expand the use of digital payment platforms across the country. The committee would be headed by Andhra Pradesh CM Chandrababu Naidu and would also include NITI Aayog Vice-Chairman and CEO and top names from the industry and academia as special invitees.

- The terms of reference of the committee include identifying global best practices for implementing an economy primarily based on digital payments and examine the possibility of adopting these global standards in the Indian context.

- The panel will also outline measures for rapid expansion and adoption of the system of digital payments like cards (Debit, Credit and pre-paid), Digital-wallets/ e-wallets, internet banking, Unified Payments Interface (UPI), banking apps, etc. and shall broadly come up with the roadmap to be implemented in one year.

- It shall firm up an action plan to reach out to the public at large with the objective to create awareness and help them understand the benefits of switching over to a digital economy and would finalize a roadmap for the administrative machinery in the States to facilitate the adoption of digital modes of financial transactions.

- The high-level group will also help identify and clear bottlenecks and provide solutions pertaining to the adoption of the steps necessary to move towards a digital payments economy.

- It will also work with all the key stakeholders for implementation of the suggested steps towards a digital payments economy and delineate and adopt measures developed by the Committee of Officers constituted for the purpose.

- Ratan Watal panel on digital payments

The panel, headed by former finance secretary Ratan Watal, was constituted in August to suggest ways to encourage India’s movement towards a cashless economy.

Way Forward

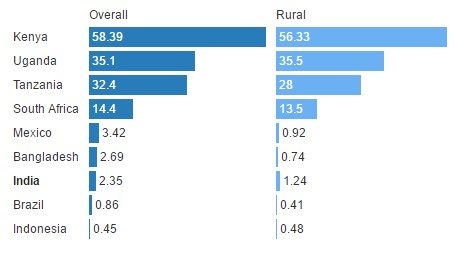

India must learn from other countries in the developing world, which have managed to reduce their dependence on cash even while bringing in more people in the folds of the formal banking system. Kenya has been a well-documented success story, where mobile money has spread much faster and deeper than in India. Kenyan households with access to mobile money were able to manage negative economic shocks (like job loss, death of livestock or problems with harvests) better than those without access to mobile money.

The path forward is clear:

- Invest in building the required financial and digital infrastructure

- A nationwide financial and digital literacy campaign accompanied by a medium-term strategy to improve access to, and awareness of, electronic payments. Targeted financial education programs can improve financial skills and credit management, and increase account ownership.

- the government must undertake the herculean task of changing attitudes towards digital payments among customers and merchants

- Put in place all necessary cybersecurity measures

Cashless Economy – What is United Interface Payments (UPI)?